ZCash Soars while Bitcoin Crashes as Saylor and a Quantum Scare Test the Cycle

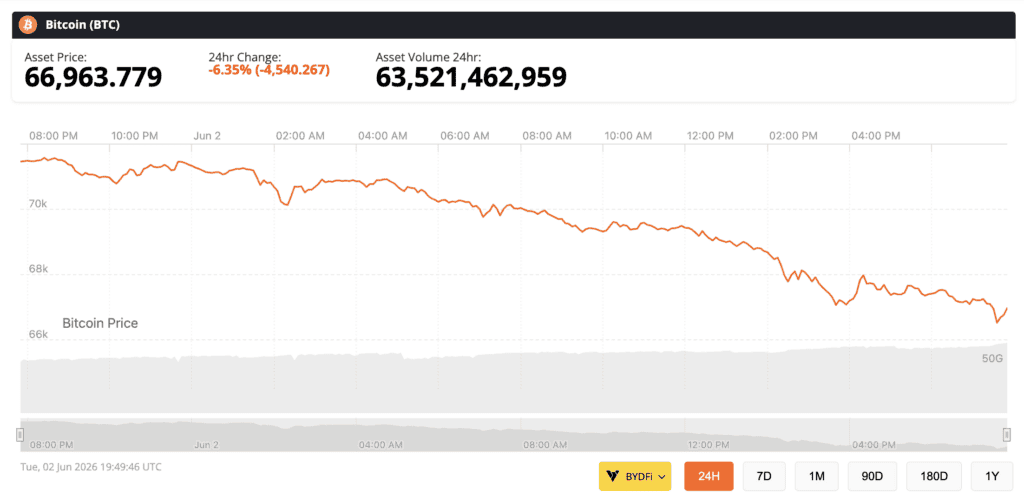

Bitcoin slid below $70,000 on Tuesday for the first time since April, touching an intraday low near $67,300 and extending a grind that has now erased roughly 45% of the asset's value since its $126,198 record last October. ZCash meanwhile, continues to outperform.

Zcash is rising, but the Bitcoin selling is the familiar kind — sticky inflation, a firmer dollar, lingering Iran risk and the largest monthly spot-ETF outflow of 2026, with around $2.3 billion leaving the funds in May. What makes this particular leg lower interesting is not the price. It is the three stories converging on top of it.

Bitcoin crashed, dropped to $66,900, source: Brave New Coin

The “never sell” line finally moved

The first is corporate. On June 1, Michael Saylor’s Strategy disclosed in an 8-K filing that it had sold 32 bitcoin at an average of $77,135 — its first sale since December 2022, and the first crack in a five-year “we will never sell” doctrine that did as much to define this cycle as any halving.

Strip away the symbolism and the trade is almost nothing: about $2.5 million against a treasury of 843,076 BTC, or roughly 0.0038% of the position. Wall Street analysts called it economically immaterial, a tactical move to fund distributions on the firm’s STRC preferred stock rather than a change of religion. In the same week the company raised more than $128 million through its at-the-market equity program, dwarfing the bitcoin sale fifty to one.

But the arithmetic is not really the point. The point is the doctrine — and the doctrine matters more now because Strategy’s blended cost basis sits at $75,699, which means its 843,000 coins are, at today’s prices, modestly underwater. That is the uncomfortable mechanic Brave New Coin flagged when Saylor first floated the idea of selling: a leveraged proxy on bitcoin, carrying around $1.5 billion in annual dividend and interest obligations, that begins selling coins to service those obligations precisely when the coins are worth less than they cost. It is the feedback loop the bears have been drawing on whiteboards for two years, and for one small filing this week it stopped being hypothetical. A pivotal STRC dividend vote on June 7 will test the financing flywheel that lets the whole structure keep buying.

A cycle that looks more like distribution

The second story is the cycle itself. Treasury firms that spent 2025 racing to copy Saylor have mostly stopped buying or started selling. Long-term holders are distributing. On-chain desks note bitcoin has spent much of the year trading below the average active investor’s entry price, and retail interest in the phrase “bear market” has spiked to a five-year high — the sort of capitulation search behavior that tends to show up near fear, not euphoria.

None of this is a structural verdict on bitcoin. It is, however, the texture of a market in its digestion phase rather than its expansion phase: the easy narratives are tired, the marginal buyer has gone quiet, and capital is rotating toward whatever still has a story. Which brings us to the third, stranger thread.

The quantum tape, and why it won’t go away

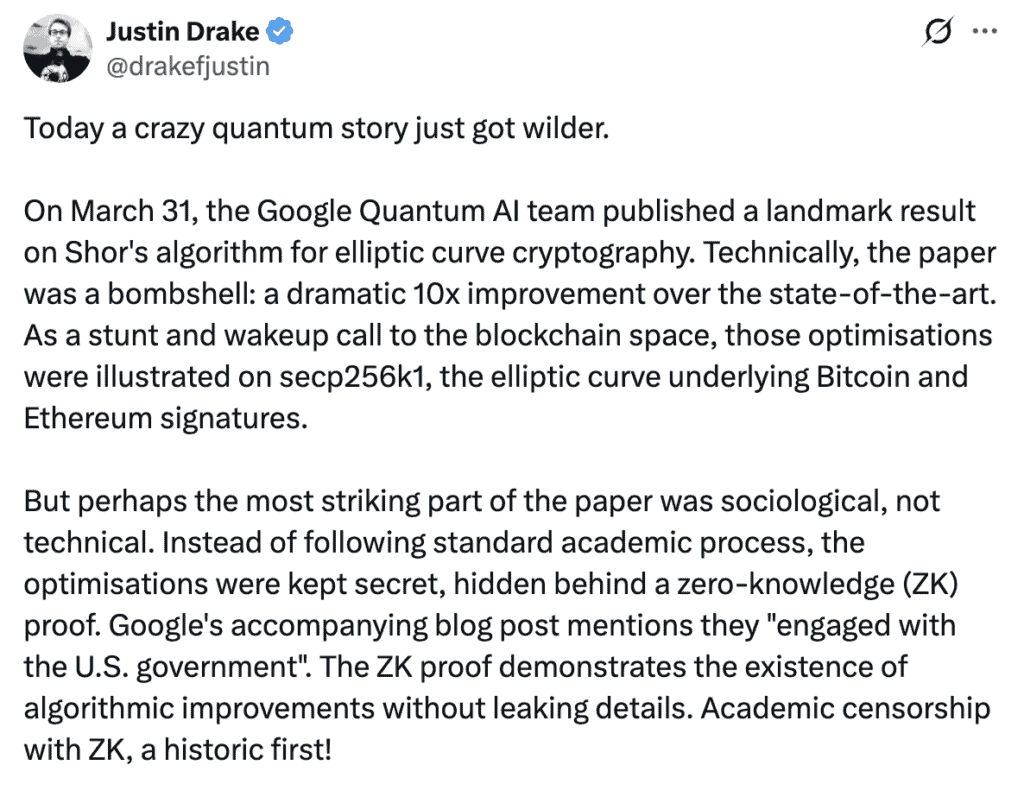

On the same day bitcoin lost the $70,000 handle, Ethereum Foundation researcher and Google Quantum AI co-author Justin Drake published a fresh thread updating his “Q-Day” odds — the day a quantum computer first breaks a piece of production cryptography. His new numbers: a 10% chance by 2030 and a 50% chance by 2032. He dismissed the U.S. government’s 2035 migration deadline, inherited from the NSA and adopted by NIST, as a date he expects to be dragged forward by years.

The quantum story got wilder, wrote Justin Drake on X

Drake’s case builds on the March Google paper that cut prior estimates for attacking secp256k1 — the elliptic curve underpinning both bitcoin and Ethereum signatures — by roughly an order of magnitude, putting the ~6.7 million BTC sitting in addresses with exposed public keys (worth north of $460 billion) inside a theoretical blast radius. A startup called Oratomic compounded the unease with a claim that neutral-atom hardware could run the attack on as few as 10,000 physical qubits. Drake, who says he spent a few hundred hours falling down the neutral-atom rabbit hole, now calls the technology “very real.”

He is careful to add the part that gets lost in the headlines: do not panic, do not rush toward immature post-quantum schemes, and treat 2029 as a sane migration target. Brave New Coin has made the same argument at length — the technical fix exists, with NIST standards like ML-DSA already published; the hard problem is whether a leaderless network can coordinate the upgrade in time. Saylor, for his part, continues to insist the risk is at least a decade out and will threaten banks and governments long before it threatens bitcoin. Both things can be true. Neither is comforting.

Zcash, the trade that decoupled

Markets do not wait for governance debates to resolve. While bitcoin has bled, Zcash has been the year’s standout: ZEC is up roughly 73% over the past month even as the broad market went sideways, trading around $545 and climbing into the top 15 by market capitalization at about $9.3 billion. The catalysts have stacked neatly — the SEC closing its long-running Zcash Foundation investigation in January, a Robinhood listing, Grayscale’s filing to convert its trust into what would be the first U.S. privacy-coin ETF, and Multicoin Capital’s disclosure of a large position. Co-founder Tushar Jain framed the bet as a “return to the cypherpunk ideals crypto was founded on.”

The privacy thesis and the quantum thesis are, conveniently, the same trade. Because Zcash’s shielded addresses keep public keys off the chain entirely, holders never sit in the exposure window that worries Drake — a point Brave New Coin examined in its case for why ZEC is one of the few altcoin theses still standing. The project is also leaning into the narrative directly, with a multi-phase post-quantum roadmap (Project Tachyon) targeting full quantum resistance by 2027, and Zcash’s Josh Swihart needling the incumbent by calling bitcoin “fundamentally broken” as private money.

Two cautions keep this from being a clean victory lap. First, the rally has not made ZEC immune: it gave back high single digits alongside everything else as this week’s risk-off wave hit, and analysts note the move has been heavily whale- and leverage-driven. Second, the irony at the center of the trade is that Zcash’s current Sapling layer is itself built on elliptic-curve cryptography — meaning the quantum hedge is, for now, a promise of future resistance rather than present immunity. The roadmap has to ship.

For the moment, though, the tape is telling a simple story under all the noise. The reflexive corporate bid that powered the last cycle is wobbling, the cycle’s own internals look more like distribution than accumulation, and a once-academic quantum debate has acquired a price. Capital is rotating toward the asset that turns all three anxieties into a pitch. Whether Zcash’s quantum-proofing arrives before the threat does is the open question — but in a market starved of stories, it is currently the one being bought.

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!