Bank of Canada draws digital currencies lessons from history

![]()

The Canadian Central Bank recently released a [staff working paper](http://www.bankofcanada.ca/wp-content/uploads/2017/02/swp2017-5.pdf) that examines the period in Canada when both private bank notes and government-issued notes (Dominion notes) were simultaneously in circulation. “Because both of these notes shared many of the characteristics of today's digital currencies,” the report states, “the experience with these notes can be used to draw lessons about how digital currencies might perform.”

The Canadian Central Bank recently released a staff working paper that examines the period in Canada when both private bank notes and government-issued notes (Dominion notes) were simultaneously in circulation. “Because both of these notes shared many of the characteristics of today’s digital currencies,” the report states, “the experience with these notes can be used to draw lessons about how digital currencies might perform.”

“History can be studied to derive lessons for private digital currencies such as Bitcoin since these currencies represent completely different units of account.”

— – Bank of Canada Staff Working Paper

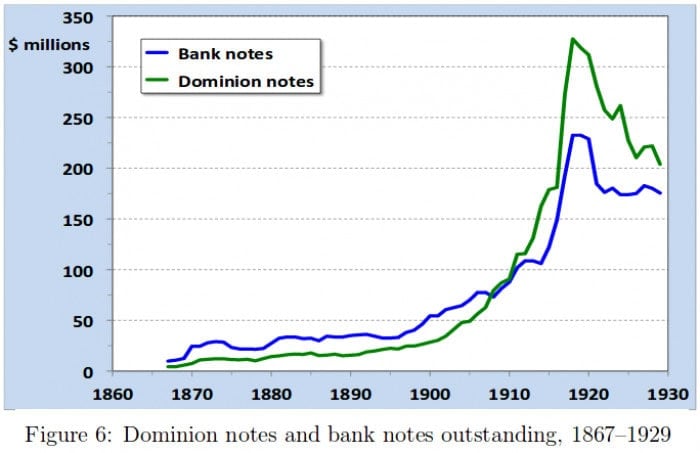

For almost 70 years, starting in 1866, Canada had Bank of Canada notes and Dominion notes. Both were replaced in the 1930s by today’s Canadian dollar, but only one of the two was issued by a central bank. The Dominion note was regional bank-issued, a series of similarly-looking bills issued by the private banks of Toronto, Montreal, and Halifax.

Both the private notes and the government notes were denominated in dollars and were widely accepted as a means of payment by persons or entities other than the issuer. The paper states that this makes them similar to present day digital currencies, which are defined as, monetary value stored electronically that is accepted as a means of payment and whose use is neither based on nor requires funds in a deposit or credit account in a financial institution. “The only difference is that in the case of bank notes and government notes the monetary value was ‘stored’ on a piece of paper instead of existing only electronically,” the paper states.

The in depth study draws five key historic lessons that might reflect the future Canadian experience with digital currencies. “Digital currencies will be counterfeited,” the report states. “One counterfeit digital currency ‘coin’ would almost certainly quickly undermine the confidence in the whole system.” Bank notes and Dominion notes were counterfeited, and given this history, it is likely that digital currencies would be subject to criminal attempts to counterfeit them.

There is an additional problem outlined in the paper, that arises with decentralized digital currencies that are not issued by a government or do not rely on a trusted third party, “like bitcoin.” The “double spending” problem introduces the possibility that someone can claim that units of the currency belong to them rather than to the person who thought they owned them. The paper notes that this problem has been solved by requiring “proof of work” or “proof of stake,” before a block of transactions can be added to the blockchain.

“Digital currencies likely will be scarce,” is the second lesson in the report authors. Central banks today have the power to issue their fiat currency in any amount, but are typically committed to keeping inflation low and stable. Given these commitments to low and stable inflation, it is reasonable to assert the growth rates of central bank digital currencies will not be very high.

Private digital currencies, the BoC argues, are likely to be scarce only when subject to strong government regulation or when there are rules for issuance hard coded from the beginning and not subject to any changes.

“The algorithm that determines the rate at which new bitcoin is created cannot be altered. Without such rules, we view it as unlikely that a private digital currency would ever enjoy wide spread acceptance or even be valued at all.”

— – Bank of Canada Staff Working Paper

The third lesson is that, “digital currencies will not be safe, although government intervention can help.” Fractionally backed digital currencies that are redeemable on demand are most like the Canadian notes studied, the paper clarifies before statting “no fractionally backed financial instrument that is redeemable on demand, whether issued by a private entity or the government, can ever be perfectly safe.”

“In the case of private issuers, there is the possibility it will fail,” the report explains. “There is some evidence that tokens can disappear and become valueless.” However, the historical experience with Canadian and United States banknotes also shows that private digital currencies can be made perfectly safe with government intervention, although it cannot be achieved solely through regulation.

The Fourth lesson is that, “digital currencies will not be a uniform currency without government intervention.” Both Canada and the United States had periods in which there was no mechanism in place to effect the par exchange of bank notes and thereby make them a uniform currency. Without such a mechanism, the paper states, exchange rates between media of exchange can deviate from par and the deviations can vary by the identities of the respective issuers, their locations, and the location at which the exchange is to take place: “This history suggests that the mechanism to achieve currency uniformity requires some intervention by a government.”

“It may seem obvious that a goverment digital currency would be a uniform currency,” the bank states. “No mechanism would be needed. And we would agree that is the case when there is only one government digital currency.”

The final lesson states, “a central bank can always get its digital currency into circulation, but its digital currency will not necessarily drive out private digital currencies.” The report went on to note that “bitcoin shows that it is also possible for a digital currency with its own monetary unit can arise.

“That bitcoin’s acceptance appears to growing would seem to indicate that such an alternative digital currency can become widely accepted.”

— – Bank of Canada Staff Working Paper

The Bank also revealed how it is currently fighting private currencies, which is primarily by issuing and controlling the legal tender medium of exchange. “This is due, at least in part, to its ability to declare such an instrument the sole instrument in which taxes can be paid.”

A government or central bank can always issue an instrument that will circulate as a medium of exchange, the paper argues. “This is due, at least in part, to its ability to declare such an instrument the sole instrument in which taxes can be paid.

Bitcoin’s growing acceptance appears to indicate that such an alternative digital currency can became widely accepted, the BoC states. However, no government has yet issued a digital currency, and It is possible that people may find it more beneficial to use the central bank digital currency than these other digital currencies. “It is unlikely that bitcoin, or any other private digital currency that has it own monetary unit, will drive out central bank issued digital currencies,” the bank claims.

“We conclude that well designed and managed private digital currencies could circulate widely but only with appropriate government regulation to ensure their safety, soundness, and uniformity.”

- Bank of Canada Staff Working Paper

Canada has long been one of digital currencies’ biggest adopters, citizens of the country have some of the best access on Earth to buying bitcoin, with merchants at over 6,000 Flexepin retail outlets, and over 140 Bitcoin ATMs.

The Royal Canadian Mint experimented with an early digital currency called the MintChip in 2012. The Royal Canadian Mint designed MintChip to be the first regulator-friendly digital cash platform, but it required expensive, proprietary hardware to be accepted at merchant shops, and didn’t gain acceptance at the time. By 2016 the Mint had sold the concept to a private company, who has since rebooted the concept with a smartphone app.

In 2013 a Vancouver coffeehouse named Waves was the first place in the world to showcase a Bitcoin ATM. The following year, the Candian government was the first to talk to a representative of the Bitcoin community in an official capacity, when Andreas Antonopoulos addressed the Canadian Committee on Banking, Trade and Commerce.

Last June, the Bank’s Senior Deputy Governor Carolyn A. Wilkins made remarks about the evolution of the space and how blockchains and digital currencies of several types would be creeping into use in Canada. The prospect of an external, decentralized digital currency like bitcoin taking off with the mainstream however, she finds ”highly unlikely.”

“People have not widely embraced digital currencies like Bitcoin because these currencies cannot outshine the competition when it comes to serving as a store of value and a medium of exchange,” states Wilkins. “Most that could happen is that national currencies and digital currencies coexist.”

While Wilkins is looking forward to the benefits that blockchains bring, such as in trade finances and being a post-trade settlement system, she noted that the technology has many hurdles to clear first, including scaling and governance issues. She then used the example of Bitcoin’s scaling issues as an illustration of how distributed ledgers need the help of government. “Protocols may be an area where governments can contribute,” Wilkins said. “In the early days of the Internet, governments helped develop the first networking protocols.”

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!