The Bitcoin ETF was an historic moment, so what happens now?

![]()

After the approval of a long-awaited Bitcoin ETF, do U.S. investors finally have an easy means to invest in Bitcoin? What is the likelihood that a Bitcoin spot based ETF will be approved? We assess the evolving Bitcoin ETF landscape in the U.S.

On October 18th, 2021, Maryland-based ProShares launched the ProShares Bitcoin Strategy Exchange Traded Fund (ETF) for trading on the NYSE Arca. This was the first Bitcoin ETF to be approved for trading in the United States. The ETF trades under the ticker BITO. The ProShares ETF is a futures-based product that tracks the price of Bitcoin CME Futures.

The launch was viewed as a significant step in the legitimization of the crypto asset industry. It has opened the door to an eventual pathway for the wider American investment community to invest in Bitcoin. Since 2014, the U.S. Securities and Exchange Commission (SEC) had routinely rejected every Bitcoin ETF application filed. The SEC reluctance to approve a Bitcoin ETF was due to concerns that investors were not adequately protected from the risks of the nascent Bitcoin trading markets. This Twitter thread from 2019 following the rejection of a Bitwise ETF explains the SEC’s thinking at the time. It shows the slow and deliberate process involved.

Now that a Bitcoin ETF is available to investors in the United States, the cryptocurrency market is set to expand in scope and relevance. Retail investors now have a more tax-compliant form of investing to get cryptocurrency exposure, and Bitcoin can now more easily be added to 401ks.

For institutional investors, an ETF will provide the deep liquidity needed to exit and enter positions without going through messy over-the-counter (OTC) services. They don’t need to worry about custody or securing assets in digital wallets. Although there are effective key management and custody services for large crypto investors in the country, an ETF will provide a more familiar and accessible pathway into crypto for large investors in the United States.

The first Bitcoin ETF opens to massive fanfare

Demand for the BITO has already exceeded expectations. Upon opening for trading, it broke the record for the largest day-1 ETF launch ever by natural volume. BITO assets under management (AUM) hit US$1.1 billion after its 2nd day of trading, making it the fastest ETF to get to $1b, breaking an 18-year-old record previously set by gold by one day. The fund’s price rose to $41.94 at the close of trading, up 4.9% from the initial $40 net asset value. Demand in the United States to gain exposure to BTC is clear. Interestingly, market observers have said that much of this initial demand for BITO came from retail markets, and there were very few large orders—referred to as “block” trades—of the size that institutional traders deal in.

The launch of the first-ever Bitcoin ETF in the United States was the trigger that pushed the price of Bitcoin to new all-time highs. A number of large investors tried to front-run the launch of the ETF and once it was launched markets were sent into a buying frenzy. Over the last three months, the price of BTC has risen by ~53%.

When markets opened for the new week’s trading on Monday, October 18th at 00:00 GMT the Bitcoin price was US$61,350. A few days later on October 21st, post the launch of the ETF for trading, the BTC price hit US$67,250.

On October 18th, the day of the ETF launch, ‘Bitcoin ETF’ was the sixth trending Google Search term in the United States just below searches for ‘Kanye West’.

Source: Google Trends

The structure of the Bitcoin ETF

An ETF is an investment vehicle that tracks the performance of a particular asset or group of assets. ETFs allow investors to diversify their investments without actually owning the assets themselves.

For individuals seeking to speculate on the price of an asset or asset class, without the hassle of custody or trading across different marketplaces, an ETF is a simple solution. An ETF can represent a basket of multiple stocks, stocks that trade in other countries, or a paper version of a physical commodity.

The objective of the ProShares Bitcoin ETF is “to provide capital appreciation.” You can’t make payments with BITO shares like you can with actual BTC, it has no currency attributes. It simply exists to rise in value, provided that BTC itself rises in value.

The fund achieves this capital appreciation through managed exposure to CME Bitcoin futures contracts. The fund does not invest directly in Bitcoin. It is a futures-based ETF and not a spot-based one where the ETF provider actually buys physical assets to back the underlying shares. This has created some concerns for market participants and observers.

U.S. Securities and Exchange Commission (SEC) Chairman Gary Gensler has signaled his support for a futures-based ETF since August. Gensler specifically endorsed a narrow form of ETFs that invests in futures contracts that trade on the Chicago Mercantile Exchange and register under the Investments Company Act of 1940. Gensler said this type of ETF “provides significant investor protections.”

The Investment Company Act of 1940 regulates investment funds, including mutual funds, closed-end funds, and ETFs. The act seeks to protect the public by legally requiring disclosure of material details about each investment company. It also places some restrictions on certain mutual fund activities such as short-selling shares.

During an interview with CNBC, ProShares head of investment strategy, Simeon Hyman, provided some insight into why the ProShares Bitcoin Strategy ETF was the first ETF to be approved. Hyman said the volume on the CME trades at a significantly higher volume than the largest U.S. crypto exchange.

He says this helps ProShare CME futures-based products more closely follow Bitcoin reference rates, an aggregate of the US dollar BTC price on several spot exchanges.

The daily volumes for Bitcoin futures on the CME currently sit at around US$6.49 billion. The top BTC/USD spot market is operated by mega-exchange Coinbase, its daily volumes currently sit at ~US$1.1billion. These numbers back up Hyman’s comments.

Source: Skew Analytics. CME futures Bitcoin volumes are heating up

An often-cited reason for the rejection of spot-based ETF applications is market manipulation. Using CME Futures as the basis for an ETF also helps to protect against this.

“It’s very difficult, if almost impossible to try to manipulate the futures market,” Hyman explained. “The combination of the CME and the CFTC is really a valuable piece of that ecosystem and the clearing house mechanism makes sure that nothing funny happens in the futures market.”

Another key factor is that CME futures are cash-settled. There is no actual custody of Bitcoin in the CME Bitcoin futures market. This means that if the SEC had any security concerns around the custody and storage of Bitcoin, these are also cleared.

The next wave of Bitcoin ETFs

Following ProShares lead, several other ETF providers are set to launch their own Bitcoin futures-based ETFs. The Valkyrie Bitcoin ETF launched on October 22nd. Invesco, VanEck, and Galaxy Digital are all set to launch their own ETFs in the coming days and weeks.

This sudden competition will lead to a price war in the U.S. Bitcoin ETF market. Investment firm Van Eck has lodged a filing with the SEC to launch an ETF called the Bitcoin Strategy ETF that will trade with the ticker XBTF. They hope to launch with a 65 basis points (0.65%) fee. This number is a considerable reduction on the 95 basis point fee charged by both the ProShares Bitcoin Strategy ETF (BITO) and Valkyrie Investments’ Bitcoin Fund (BTF).

While the BITO has a clear first-mover advantage, if XBTF is able to offer a significant price advantage then traders will likely make the shift to the newer entrant.

The futures-based ETF- is the market getting an inferior product?

An ETF based on futures can create problems when markets are in a state of Contango, a situation where the futures price of an asset is higher than the spot price of an asset.

Issues may arise for Bitcoin futures ETFs because the funds will need to renew or “roll” their futures contracts that back the ETF shares regularly. If the price of the longer future contract that is being rolled into is higher than the price of the expiring contract, the ETF issuer needs to pay the difference between the two contracts. Meaning they have to bear a loss known as the Contango bleed.

In 2013, Motley Fool warned against buying the United States Natural Gas ETF because it had been trading at a loss against the spot price of natural gas. At the time of the Motley Fool article, the United States Natural gas ETF stood to lose 1.5% in a single months’ futures roll.

Contango, a premium on the futures contract vs the spot price, can often occur with commodities that have complex custody requirements. This is because of their ‘cost of carry’, or any charges an investor would have to pay for holding an asset over a period of time. The cost of carry can include depreciation due to spoiling or it can involve the storage costs of handling an asset.

If investors expect the price of an asset to rise in the future and it has a high cost of carry, they are willing to pay more for it in the future. BTC meets both these requirements and as such its futures price often trades at a significant premium to the spot price.

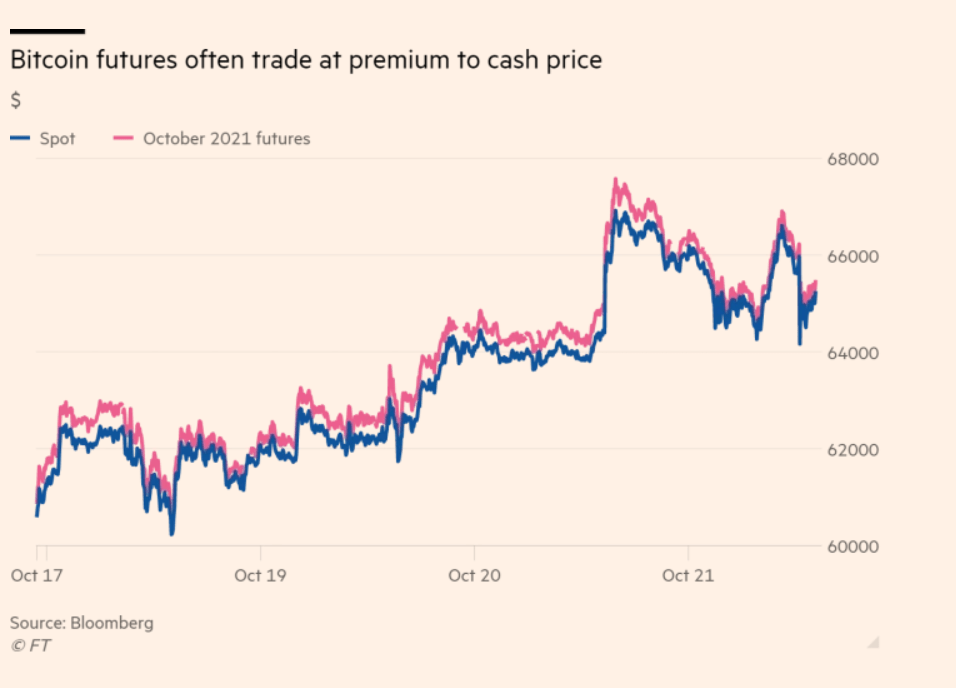

Source: FT.com

How much a futures-based ETF may be affected depends on the size of the market of the underlying asset. In traditional finance, high-frequency traders move in rapidly to take advantage of the difference in price between futures and spot. These arbitrage opportunities quickly shrink the price gap.

In the Bitcoin and cryptocurrency market, however, there are still far more retail players than institutional players meaning there is generally not enough big-money capital to close the gap between the futures price and spot price.

A “simple cash and carry trade” selling futures from the CME and buying spot Bitcoin can provide an annualized return of ~30%, Stéphane Ouellette, the chief executive and co-founder of Canadian hedge fund and broker FRNT, told the Financial Times. The gap is large and does not look like shrinking any time soon. This meaning Contango may persist in Bitcoin leading to ETF providers needing to pay heavily to roll contracts and the prices of Bitcoin futures-based ETFs may potentially trade at a lower price than spot Bitcoin.

Charlie Morris of ByteTree Asset Management says he expects the BITO ETF to underperform spot BTC by 8.4% annually, before fees.

At ProShares, Simeon Hyman responded to Morris’s analysis on a podcast. He says he estimates that the roll cost for the ETF would be ~2.5% and says a highly likely expansion of the Bitcoin market could further reduce the Contango bleed. Hyman says with other assets the bleed could be an issue, however, because of the optimism surrounding the future price of Bitcoin, investing in the ETF will still be worth it for many investors.

Source: Twitter

The above chart tweeted by Eric Balchunas, Senior ETF Analyst for Bloomberg, indicates the preference for a physically-backed Bitcoin ETF as opposed to a futures-based one in the Canadian market.

A physical Bitcoin ETF does not have to deal with the same Contango-based challenges a futures one has to. It is more likely to closely follow the actual spot price of Bitcoin, futures-based ETF issuers have to pay for the futures contract roll-over and this affects the ability for them to offer a product that efficiently tracks the price of BTC or they need to charge a higher fee for their ETP.

Michael Sapir, chief executive of ProShares, defended BITO’s 95 basis point fee in a quote shared with the Financial Times he argued that the fund was actively, rather than passively managed, with ProShares’ traders “applying our expertise to roll the [futures] contracts”, rather than doing so automatically at a fixed point before expiry.

It is likely that the market would prefer a physical Bitcoin ETF, however, most analysts and observers don’t believe it will arrive until the second half of 2022 at the earliest.

Speaking at Yahoo Finance’s All Markets Summit on Monday, Gary Gensler drew a distinction between the spot version of Bitcoin and the futures version trades on the CME that falls under the regulation of the Commodities and Futures Trading Commission (CFTC). “It’s a matter of bringing as much of this space within the investor protection remit,” Gensler told Yahoo Finance.

Earlier in his interview for the conference he said he still has concerns about the investor protections in the ever-growing cryptocurrency financial markets, “Investors aren’t protected the way they are, whether they go into the stock or bonds markets that we’ve overseen so long,” said Gensler at Yahoo Finance’s All Markets Summit Monday. “Without that, I think it really is, as I’ve said to others, a bit of the Wild West.”

Conclusion – A step in the right direction

The first step in Bitcoin’s American ETF journey has begun. It has been undeniably successful in breaking long-held ETF volume and assets under management records. The launch and anticipation of the ETF created positive buying pressure in the wider crypto market.

The SEC approving an ETF for launch, after five years of continual application rejections, pleasantly surprised investors. Market euphoria has faded in the last week, however. One reason for this may be because the ETF applications that have been approved have had to make major compromises that affect their efficiency.

The futures-based ETFs currently trading in the United States on the NYSE-Arca are backed by the biggest derivatives clearinghouse in the world, the CME. The large volumes on the CME mean their markets, in comparison to spot markets, are less likely to be manipulated. CME futures are also cash-settled meaning the messy business of Bitcoin custody is bypassed.

The nature of futures markets and the issue of ETF issuers needing to manage contracts behind the scenes means that there are inherently going to be differences in these ETFs and the spot price of BTC.

It is not simply a 1-for-1 ‘paper version of BTC’ that many people expect. It appears likely that these futures-based Bitcoin ETFs will trade at a loss to spot BTC.

With a physical Bitcoin ETF not likely to be approved anytime soon, the market will have to make do with these inferior ETFs for the immediate future.

Nonetheless, the launch of the first Bitcoin ETFs remains a net positive for the space. It significantly opens up the opportunity for investors in the largest economy in the world to gain exposure to Bitcoin. The ETFs are tradeable on the biggest cross-asset marketplaces in the world and will have much simpler tax obligations than physical Bitcoin.

Even if these ETFs underperform spot Bitcoin, if the asset maintains its ability to achieve oversized gains versus legacy finance assets this will likely not matter to most Bitcoin ETF investors.

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!