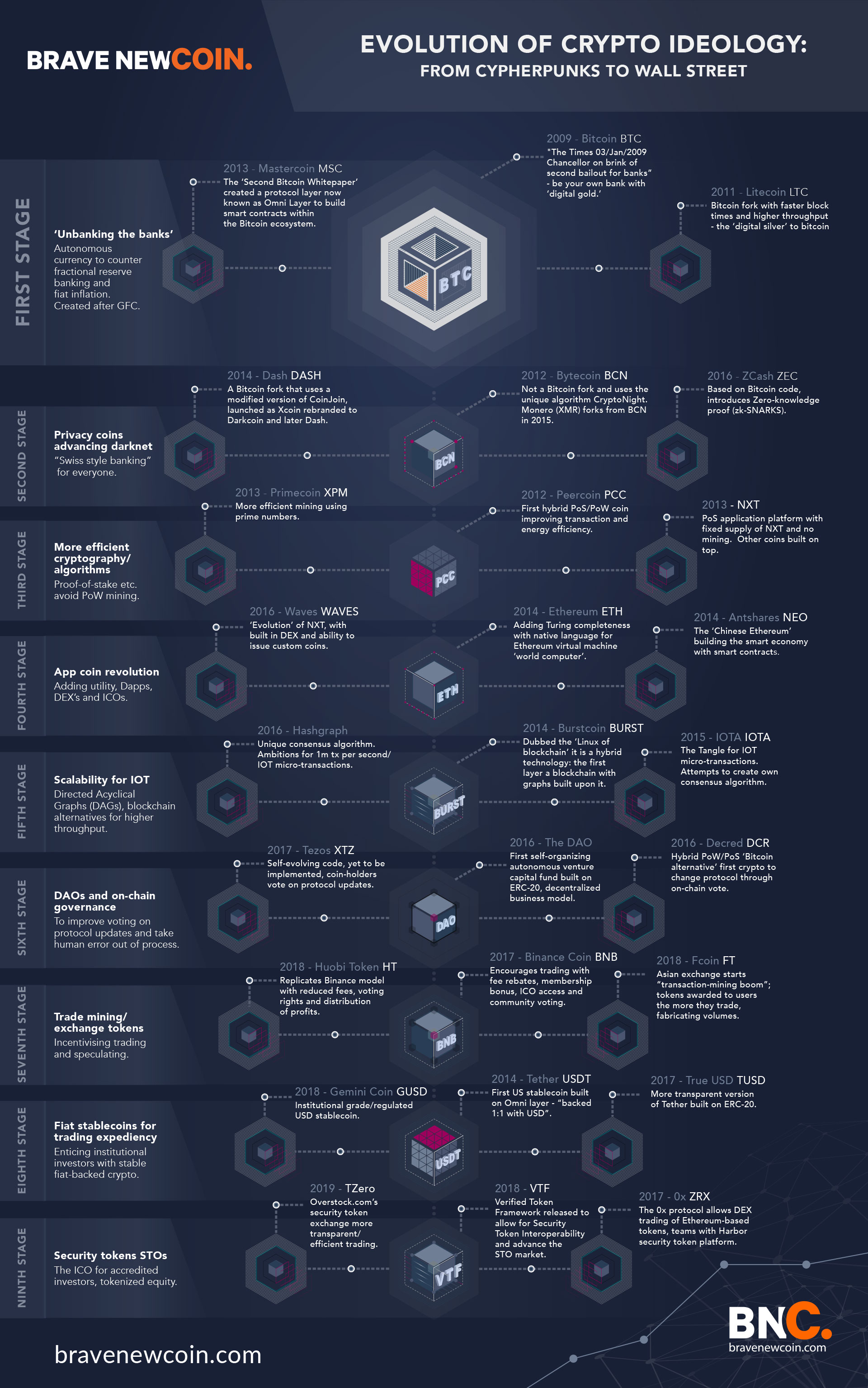

How blockchain is reshaping our economic, environmental and social orders Pt I

![]()

In this series we look past 2020 to what the future holds for crypto beyond fiat-pegged stable coins and speculative prices to the original ethos of crypto and the cypherpunk movement - to redesign our economic, social, political and environmental structures . We also explore why we need to decouple the dual role of store of value from medium of exchange from common currency in the future and why bitcoin and cryptocurrencies provide a unique opportunity to break the debt cycle created by fiat and banks.

Reforming the capital markets will be the first step for blockchain technology but this is an incremental step when we look at the role cryptocurrencies will play in the move from a world operating beyond capacity in the pursuit of exponential growth to a steady-state of growth.

Although currently going through an identity crisis, cryptocurrencies do have the power to "democratize money" and "unbank the banks" as intended by Bitcoin but not in the way that most people are expecting.

It won’t be through speculating on digital assets or the proliferation of ETFs and ICOs, innovations in trading platforms, DEXs or the newest algorithmic strategy. Instead, cryptocurrencies will change our world by expediting our way out of the "credit epoch" that has been prolonged by expanding government balance sheets and inflating assets to keep GDP rising to an epoch of lower growth and less consumption.

For centuries, money’s dual role as a store of value and medium of exchange has been dichotomous as the labour class use money to survive and the financial class use it for economic rent by lending it to the workers. This conflict has led to a perversion in government policy and left the working class beholden to interest rates that they want kept low so to afford servicing their debts while the moneyed class want them high to earn the best return on their idle capital.

This dual role has also made national currencies toys for colossal speculation with economic and humanitarian consequences every year. Over $1.3 trillion is traded per day in currency markets, dwarfing the value of the world’s stock markets combined, and 96% of those transactions are purely speculative. This has led to the infamous "Soros" style attacks on weaker currencies that has precipitated several of the recent credit crisis in developing economies from Argentina to Mexico.

The stages of currency:

- Commodity-based: Grain, cattle

- Fiduciary: Precious metal, gold/silver

- Fractional reserve: Expands money to be more responsive to supply/demand

- Credit: Current system perpetuated by debt issuance and debt servicing

- Crypto future: Millions of local and micro economy currencies in a circular economy

Over the centuries currency has undergone different stages of debasement in what some define as Gresham’s Law whereby the incumbent (good quality) currency is replaced by the new form of money (lesser quality) coming into the economy at the same face value. People would rather spend the lower quality new currency and save the old so its velocity accelerates until the old is squeezed from the system.

"All money is a matter of belief" – Adam Smith

This process has led to the dilution of currencies from commodities like cattle, grains etc to metal coins (silver, gold, nickel etc), which in turn were diluted in metalic content to create more of them, then to "worthless" fiat paper and eventually to fractional reserve and credit that is merely bits on a computer.

With cryptocurrencies we have a historic opportunity to decouple money’s dual mandate as a store of value and medium of exchange and dilute, if not reverse, the importance of national fiat currencies to create millions of more tangible local and regional currencies backed by physical assets and common natural resources (minerals, metals, air, land). These sorts of currencies have been tried before but never with the power of blockchain.

I. How we got here: From industrial to finance capitalism

Credit has been around for millenia since the first farmers extended it in a form IOU between harvesting cycles. A credit/debt cycle is created any time a person or country borrows money and, like any cycle, it gathers momentum with each completion.

Former US economic advisor and independent economist, Michael Hudson, points out that "most debt in today’s economies is taken on to buy real estate (commercial and private) and financial securities. Within the industrial sector, most corporate debt is taken on for leveraged buyouts of smaller or impaired competitors."

Our current version of ‘casino’ credit has inflated asset prices since the 80s and is the antithesis of the founding industrial capitalist vision of bringing prices and incomes in line with their cost-value.

Industrial capitalism replaced the feudal landlord system of the middle-ages in the 19th and 20th centuries by taxing away ‘unearned income’ from the commonwealth such as land (ground-rent) and natural resoures. However, this same rentier system has re-emerged as finance capitalism, where one class is renting out excess capital out to another to work for their return on investment.

How banks tried to replace the business cycle with a debt cycle

Banks make their money in the margin between the rate they borrow money and rate at which they loan it out, known as the interest rate spread, and they have amplified the effect of business cycle booms and busts by extending credit and expanding "money" in the system during good times and contracting in bad times.

John Maynard Keynes observed the perversion of the credit model when he remarked in Economic Consequences of Peace that the fiat credit system is designed with the intent of growing an economic cake that is never intended to be eaten.

In other words, we haven’t been eating our share of the "cake" but putting it towards the rest of the collective mix so when we do actually need it we take an even smaller slice as we delay retirement later and later.

As the average age of retirement in the US keeps rising it has also assisted in GDP growing year-on-year.

A corollary to the rising retirement age, GDP growth which for years has moved in tandem with household income has decoupled since the mid-1980s and grown while wages have stagnated.

The breakdown of the traditional correlation circa 1986 between US income and GDP growth has been dubbed the "Great Decoupling". Source: World After Capital.

This GDP ‘growth’ is a euphemism for debt and it is only growing because people are taking on more debt to service old and buy more, growing exponentially since the 1980s. Until recently Ireland held the mantle for the most indebted households at over 115% of GDP, fuelled by the real estate boom and bust, but Australia has blown that away with household debt of over 120% of GDP, again fuelled by property speculation and the most lenient credit conditions for decades.

Household debt globally has taken off since the mid-1980s. Bank of International Settlements data, graphic Prof Steve Keen.

To get itself into such a position, Australian banks have manipulated credit terms in all sorts of ways to expand credit/debt such as the short-term "interest-only loans" to fantasy accounting that budget the cost of raising a child in Sydney at $7 a day.

However, since the Royal Commission into Australian banking practices uncovered rampant malpractice ranging from racial predation to charging dead customers for financial advice, the banks have reigned in their credit and Australian house prices are plummeting, down 10% alone in Sydney this year.

Just how indebted are we? Look at the monetary base

To put it in context, U.S. households have about $8 trillion in mortgage debt, over $1 trillion in auto loans, over $1 trillion in student loans and nearly $1 trillion in credit card debt. U.S. business debt is a total of $25 trillion, of which about $15 trillion is in the financial sector and $10 trillion in non-financial businesses.

M1 is the money supply that includes physical currency and coin, demand deposits, travelers checks, the most liquid portions of the money supply. M2 is a calculation that includes all elements of M1 as well as "near money" such as savings deposits, money market securities, mutual funds etc.

In the US the government has stopped tracking the larger monetary aggregates, such as M3 and only using narrower measures, such as M2, making it hard to gauge the actual growth of the monetary base. Nonetheless, by the M2 measure alone the monetary/credit base has been growing by about $1 trillion annually over the last decade, and the actual amount of money created in the economy by quantitative easing is likely to be much greater.

A similar expansion of the monetary/credit base has happened throughout the world. Globally, there is $250 trillion in outstanding debt and four times that amount in unfunded liabilities, not to mention the massive amount of tangled financial derivatives roughly the same size as both those debts and liabilities put together.

II. Where we’re going: Money ‘for the people’ and digital sovereignty

Bitcoin and cryptocurrency’s original cypherpunk ethos was to "unbank the banks" with an alternative currency to the debt edifice our economy has become in the age of credit and fiat.

One way cryptocurrency could obviate banks is by filling the gap between the needs of the lendee and that surplus of the lender – the traditional staples of banks, car and home loans, will be in less demand as the economy becomes more decentralized. We’ve experienced the first stages of decentralization with Uber and Airbnb but this trend will only continue as the sharing economy grows and people earn on their own terms bartering with hundreds of different types of cryptocurrencies outside the remits of income tax or interest.

Currently, we are all chasing one deonomination of currency for all different uses and this is what drives banks’ (and central banks) margins. In the near future we will have an ecosystem of many cryptocurrencies for applications existing on digitally sovereign decentralized platforms on the internet and outside the jurisdiction of governments and central banks. These currencies will diminish the power that central bank deposit rates have on our lives and even more so squeeze the margin of commercial banks from the current positive risk-free interest rate to lend at even lower negative rates that we’ve seen before (think -2 or -3%) as central banks are forced to charge for money kept on deposit.

Crypto and digital banks will dilute the importance of banks’ positive interest rates among young savers

The cutural obsession of saving money with banks has been waning with younger generations as all they’ve known in their lifetime is a falling interest rates and paltry returns on their deposits.

For those in the Baby Boomer generation, which enjoyed double digit interest rates for decades, there was reason to believe in the ‘miracle of compound internet’ but for the millennial generations who have the lowest rate of savings of any generation for their age in history, the idea of putting your money for returns of 1-2% with a bank is anachronistic.

According to one piece of research, 67% of "young millennials" – those between 18 and 24 years old — have less than $1,000 in their savings accounts and 46% have $0. Older millennials, those between 24-35 didn’t fare much better, 41% of whom had no savings.

The secular downtrend in interest rates since the early 80s also marks the point when credit-fuelled economic growth started to replace real growth. The interest rate fell to a historic low during the GFC in 2012 and 2016 at just above 1% (and lower for many banks’ own interest rate) and knowing that it has run out of rope before the next recession hits the Federal Reserve has been hiking rates rapidly this year to get to them to a point where they can be effectively lowered again – ironically this is what many "experts" believe will trigger the next recession

The interest rate of the Ten-Year Treasury (T-Bill) that has the most impact on short-term interest rates at banks has been in a secular downtrend for decades.

Automation will compound secular deflation and bring interest rates back to negative territory

The internet has for the first time in history created the possibility of zero-cost marginal production – goods that require no staff or overheads to produce – which will have a hugely deflationary effect on the world going forward.

For the past century the natural level of short-term US interest rates (effected by the Fed) has been equal with nominal GDP growth — critical to keeping the amount of debt in the world growing at least as fast as the rate of debt servicing. But when the yield spread between the short-end of the interest rate curve and the long-end starts to invert, it tends to presage a recession in a self-fulfilling prophecy of lower future growth expectations as investors pile into longer dated bonds for a long-term safe return, driving their prices up and yields down.

Although the most closely watched "recession indicator" is the spread between the 2-10 year bonds the spread between the 3-5 year recently inverted (went below 0) for the first time since 2006/7. This inversion is taken as a harbinger for recession. Source: Bloomberg

According to Hudson, over the years "the Federal Reserve was able to inflate asset prices by flooding the economy with enough credit to lower interest rates, enabling banks to capitalize a rental or corporate income at a higher multiple in lending to new buyers."

Central Banks across the world ‘expanded their balance sheets’ creating massive price inflation over the past years in stocks, bonds and real estate.

With the money the central banks paid them for bad assests, commercial banks didn’t pass it on by lending to people who would actually spend the money (middle and labour classes) they instead lent mainly to other financial institutions with a better projected rate of return, not to finance new capital formation or employment but to make capital gains by debt-leveraged speculation.

Interest rates were forced into negative territory (below a risk-free rate for banks) in recent years to combat recession, however, with each completed debt cycle central banks’ ability to spur economic growth through monetary policy has diminished.

When the next recession hits it will be compounded by the deflationary forces of automation and technology that are already long underway replacing workforce jobs and, consequently, consumer demand.

A renaissance of local and depreciating currencies in digital form

Local currencies and currencies that depreciate with time may sound like a radical idea but in fact have a long history. They were used widely in the US and Europe in the form of scrips during the Great Depression when local governments and jurisdictions issued their own alternative currency as the nation’s banks ran dry.

Depreciating currencies (known as a demurrage rate) incentivize the circulation and velocity of money instead of hoarding and get people to spend without credit or getting into debt. The most famous example of a demurrage currency is the Worgl, or Freigeld ("Free Money" in German), that decreased in value at a rate of 1% per month and stamped every time it was spent. The experiment was inspired by economist Silvio Gesell’s concept of Freiwirtschaft ("Free economy") where money free is from speculation.

The demurrage currency worked to acclaim in the Austrian town of Worgl during the Great Depression, dubbed "the miracle of Worgl" as it lifted the town from its nadir although it is very unlikely that it would have been sustained.

Colu – building local cryptocurrencies

Colu is one blockchain startup that aims to "change the face of your local economy" and has already issued community currencies in the UK aimed at boosting a community’s economic activity. It also plans to create city currencies with incentive systems to boost positive behavior among residents by rewarding social actions such as volunteering, participating in civic activities or spending their digital currency on local products.

Kintetsu Harukas Coin – corporate community coin

The listed Japanese conglomerate Kintetsu which operates a railway connecting major cities and tourist destinations issued its own pilot community currency earlier this year.

The Kintetsu coin was adopted in over 400 locations across the Kintetsu Group, including a department store chain and the Harukas observatory atop the 300 meter high Abeno Harukas tower (Japan’s tallest building — located in Osaka).

The pilot results were so positive that the company will be adopting the digital currency for 2019.

Coffee Coin – microeconomy/artesanal coin

Middlemen services like Fair Trade or bodies that certify products will be also made redundant through microeconomy crypto coins.

The organic/Fair Trade premium has long created a conflict for consumers: paying extra for staples has made ‘eating ethically’, or just eating non-chemically, a luxury. The cost of certifying as an organic grower or fair trader with the governing body shifts the cost to the customer but when supply chains issue their own currencies they can save the cost of certification and perhaps we’ll just have to trust in its provenance.

CoffeeCoin (COF) is one such utility token function within its blockchain ecosystem, CoffeeChain, as a nominal representation of 1kg of green arabica coffee on the Waves blockchain with a total supply of 40m COF.

It is connecting producers of speciality coffees in Indonesia with end buyers as well as a coffee trading platform for those in the entire chain from farm to cup. The value of the currency could be interpreted as the trust of the provenance of the goods in the system.

Cryptocurrency will finish the historic mission to create autonomous currency

The pursuit to create a currency as a medium of exchange decoupled from a store of value has been a long road and economist John Maynard Keynes was one of the earliest proponents. He asserted that the dual role of money creates conflict of interests between the "haves" and "have nots" and has attributed to inequality. He frowned on the speculative use of common currency and interest rate arbitrage and was an advocate of negative interest rates in certain cases.

In the 1940s, Keynes proposed a supranational global reserve unit of account called ‘the Bancor’, a sort of precursor to the IMF’s Special Drawing Rights. While not conceptually a currency it was to be used purely as a non-speculative unit for international trade settlement – individuals could not hold or trade in Bancor. The US had intended to adopt it but after WWII and Bretton Woods the USD was made the defacto global reserve.

Contemporary iterations in the vein of Keynes’ Bancor have also been proposed. Economist Bernard Lietaer’s Terra Trade Reference Currency (or TRC), was designed in 2000 as a supra-national complementary currency initiative, intended to work in parallel with the current international monetary system that was free of geopolitical and speculative vagaries of national currencies.

It is designed to counteract the booms and busts of the business cycle and stabilize the global economy. Most importantly, it will resolve the conflict between short-term financial interests and long-term sustainability – Terra whitepaper

TRC is a demurrage currency that depreciates 4% per annum to avoid hoarding and inventivize its use as a standardized "countertrade" unit of account for international trade.

Lietaer is a former currency trader, voted "the world’s top currency trader" by Business Week in 1992, and renowned as the "Architect of the Euro" which he intended to be used as a pan-European common currency and not intended to replace national currencies.

"[Terra is] a global complementary currency designed to provide an inflation-resistant international standard of value; to stabilize the business cycle on a global level; and to realign stockholder’s interests with long-term sustainability."

Both Keynes’ and Lietaer’s proposals have literally taken on a new life in blockchain through eponymous cryptocurrency projects the Bancor Protocol (BNT) and the Terra stablecoin. Ironically, Bernard Lietaer is the chief monetary architect for the Bancor Protocol Foundation.

DAO’s will create the first digitally native economies

Terra Money

While the recently abandoned Basis project was the most famous (perhaps now infamous) of ‘algorithmic central banks’, stabilizing currencies with decentralized assets, the endeavour to create a stable fully autonomous currency continues.

Perhaps taking inspiration from Lietar’s physical proposal, the stablecoin Terra aims to be the first non-speculative global cryptocurrency by focusing on being a medium of exchange and not a store of value to be used as the primary currency in e-commerce in Asia.

It proposes a two-token economy in which Terra is the stable coin initially pegged to a basket of currencies that reflect the IMF’s Special Drawing Rights (currently U.S. dollar 41.73%, Euro 30.93%, Renminbi 10.92%, Japanese yen 8.33%, British pound 8.09%) with additional commodities to be added to the basket such as metals, grains and decentralized assets.

It envisions a decentralized economy similar in essence to the recently defunct Basis stablecoin where its second currency ‘Luna’ is the incentive token for users to maintain Luna ‘deposits’ with the Terra foundation and rewarded with the transaction fees generated from Terra.

Terra is envisioned to become the native token for a whole ecosystem of Dapps and DAOs to use in the future as a method of payment online or at merchants point of sale.

Aragon

While not a necessarily a stablecoin endeavor Aragon is attempting to create the world’s first digital jurisdiction purely for decentralized organizations (DAOs) to operate in the same way physical organizations do, with legislation and contractual agreements.

Aragon lets you freely organize and collaborate without borders or intermediaries. Create global, bureaucracy-free organizations, companies, and communities.

Its ERC-20 token, ANT, will be the native currency of the economy and its value kept stable (but not pegged) in a similar way to Basis or Terra, by algorithmically adjusting the supply from its stability reserve.

Aragon could play a large role as communities reclaim their commonwealth (land, air, water, natural resources) from corporations a hrough the use of token-economics to move to an efficient economy.

Conclusion

The internet started the shift to a sharing economy with the open-source revolution and although it has been annexed by a few coroporate behemoths (FANG companies) it is returning to its decentralized founding vision.

This open-source ethos also fits in with the classical vision of capitalism where the rent of internet landlords of Facebook and Google was taxed away from the ownership of open resources. This shift is also embodied by regulators across the world who are fining Big Tech companies billions and strangling their ad-based business models.

The expansion of fiat-based debt has interrupted the flow of production and consumption which has led to economic shrinkage and will become more evident after the next recession hits. At that point it will be unavoidable for an entirely new economic, environmental and social order to re-emerge.

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!