Kucoin-shares Price Analysis: Shining a spotlight on IEOs

![]()

The Kucoin exchange's native token, Kucoin-shares, has emerged in the short term crypto market consciousness rising ~200% in the last month on the back of speculation surrounding Kucoin's first 'Initial Exchange Offering' (IEO),and given KCS's utility as the only liquidity option to access the IEO. Under the hood KCS has a diverse value proposition, giving access to trading fees and net profits of the exchange however recent value has likely been driven by hype surrounding the IEO ecosystem.

Kucoin-shares are the all-access membership tokens of the Kucoin exchange. Kucoin is an international exchange based out of Hong Kong that currently supports 382 pairs as per Brave New Coin’s exchange listing table.

The Kucoin exchange’s native token, Kucoin-shares (KCS), has risen by ~200% in the last month and is currently trading at ~USD 1.33. Momentum for the token has been driven by hype surrounding the first initial exchange offering sale being hosted on Kucoin. Despite this impressive short term growth KCS remains down 93% from an all time high achieved in January 2018. The platform released an updated version of its interface with a new dashboard and trading engine on February 19th 2019. It currently occupies the 54th position on BravenNewCoin’s market cap table.

Kucoin has differentiated itself from other major alt-coin focused exchanges and exchange tokens because 50% of total trading fees derived from trading on the exchange are distributed to the holders of Kucoin-shares (KCS) daily.

The distribution mechanism falls under a solution called ‘Kucoin Bonus‘ where at the end of every trading day, following an accounting process, an amount equal to 50% of that day’s trading fees is collected and then used to buy back KCS from the market. This KCS is then redistributed to holders of the exchange token based on the size of their holdings.

The formula used to calculate the size of the bonus is 24 hour Total Transaction Volume on Kucoin * 50% * (User Holdings/100000000). The minimum amount required to receive Bonuses is 6 KCS which is equal to ~8 USD in today’s prices.

The current yearly staking return when holding a minimum amount of KCS is ~2%, while monthly returns are 0.16%. Based on current 24hr volumes of Kucoin, holding a 100 KCS would return 1.95 KCS per year which in today’s prices equates to a ~USD 133.1 investment yielding ~ USD 2.61 return.

The Kucoin-shares token also has other utility beyond access to the Bonus. Users holding at least 1000 KCS receive a 1% discount on fees, while holding 10,000 KCS gives access to a 10% discount and holding 30,000 KCS results in a maximum 30% discount.

KCS is also useful as a liquidity tool and a medium of exchange to onramp onto other crypto assets, and the value of Kucoin-shares increases the more tokens it is paired with. Currently the Kucoin exchange’s three most popular pairs are all KCS based (KCS/ETH, KCS/USDT, KCS/BTC), suggesting holders are using it for one of its intended purposes as a liquidity tool.

Similar to the Binance exchange’s BNB token, KCS has functionality similarly to equity, with net profits earned by Kucoin redistributed to KCS holders in the form of a token burn, functioning in a similar manner to a dividend. Every quarter the exchange uses 10% of net profit to buyback KCS from the market, making each existing token worth more by artificially reducing supply

The most recent buyback, Q3 2018, was worth 196,211 KCS worth ~USD 219,756 based on the KCS value at the time of the buyback. This suggests that Kucoin’s profits for the quarter were ~USD 2 million. The exact date of the buyback was announced 3 weeks before it actually happened – likely to create speculative buying activity around the buyback date.

For reference, Binance Coin’s Q3 2018 quarterly token buyback, burnt ~USD 6 million worth of BNB which suggests estimated profits of ~USD 81.4 million.

KCS’s core point of difference and primary value driver is its Bonus feature, which on paper is a way to long the entire crypto market. Initially when Kucoin Bonus was launched, trading fees would actually be redistributed in their original denominations, so for a given trading day’s amount of BTC/ETH trading, a user would receive small amounts of ETH and BTC based on the Bonus calculation.

Users received tiny amounts of each crypto based on all trading between pairs but denominations were so small that it was somewhat useless and difficult to fill orders to sell. Kucoin also does not have a dust collection tool, Kucoin made the switch to only KCS payouts for bonuses in July 2018.

KCS value is set to expand in the near future, with the upcoming release of Kucoin Spotlight, the exchange’s own Initial exchange offering and a direct counterpart to the highly popular Binance launchpad platform.

The first Spotlight sale, the MultiVac project’s MTV token, is set to occur on April 3rd. Multivac is a fully sharded blockchain that has already garnered a USD 15 million war chest from round A investments from a group of prominent blockchain project investors including Arrington XRP.

The sale will be for 600,000,000 MTV tokens, worth ~USD 3.6 million, with each token initially selling at USD 0.006. The IEO sale will be for 6% of total supply of MTV tokens and tokens will be allocated on a first come first serve basis and will only be accessible with KCS.

Initial Exchange Offerings are ICO style token sales held exclusively on single exchanges. Before exchanges and the project team goes through with the public token sale, the exchange platform undertakes a thorough review of the project using verification conditions to ensure the project is robust enough to be sellable to the exchange’s buying public.

Projects can only access users who are vetted by the exchange’s KYC/AML system. Since most IEOs are happening on regulatory arbitraging Asian exchanges, these requirements tend to be basic. There is a natural incentive to not list scam projects because the exchanges have reputation and occasionally skin in the game, so have something at stake when listing tokens.

Source – CryptoPotato.com – What Is an Initial Exchange Offering (IEO) and How It Differs From ICO?

This means at least at face value to retail users, IEO projects have been through a degree of vetting before being sold to the public and may be safer in some ways than traditional ‘direct to the public’ ICO models.

The major advantage of IEO’s is that the newly issued tokens are immediately tradable by initial buyers, which makes these issuances immediately attractive to short term ICO traders who see the pre-launch hype of tokens as set-ups for swing trades. Potential trading profits are not held by token lock-ups or by the lack of a liquid market to sell back to.

Token projects also don’t have to go through the stressful process of trying to find exchanges willing to list a new token or paying listing fees, particularly if the IEO occurs on a well known exchange like Kucoin, Binance or Bittrex. Running a public sale on an exchange means immediate access to a pool of willing participants, and this limits marketing and promotion requirements for the token projects.

There is a limit to the number of tokens participants can buy in an IEO to ensure some level of fair distribution. An early innovator of the IEO concept, Binance, only runs around one token sale a month. This means retail investors/exchange token holders are not bombarded with a cavalcade of complex blockchain project ideas, and increasing the FOMO appeal for individual IEO tokens by giving the publicly sold token projects an element of prestige and rarity

However, while IEOs offer a number of advantages from a financing and liquidity perspective, the system is not bulletproof. Participating in an IEO requires that a user leaves a large amount of crypto on an exchange, and in the hands of an exchange’s blockchain wallets. This is a security risk because exchange hacks do happen. The black swan event of a major hack happening during a token sale has the potential to derail the currently positive sentiment surrounding the security of this system of token fund-raising.

There is also the general thought in old skool crypto circles of ‘not your keys, not your crypto’ meaning the heavily centralized IEO ecosystem, where multiple user funds are managed by a single exchange via their exchange accounts, is likely to continually face criticism from decentralization fans. ICOs use smart contracts, whereas IEOs operate more like a direct transfer meaning ownership transfer is less robust.

Other challenges include regulation. Regulatory crackdown from agencies like the SEC in the US dampened enthusiasm for ICOs in 2018 and funding for the sector quickly dried up as investors became acutely aware of the potential tax implications and legal challenges for ICO projects. Currently most IEOs are run by Asian exchanges, with access to them from regulated regions like China, the US and New Zealand blocked. If regulators in currently accessible IEO markets decide to up their requirements for IEO sales, this may limit their scope and wider enthusiasm.

A number of Binance Launchpad sales have also had bottleneck issues and server overload challenges, which has often meant participating in IEOs has been a frustrating experience where users have felt like they were in limbo and unsure if they had been allocated tokens.

Nevertheless IEOs have revitalized the crypto token public raising space by streamlining and adding liquidity to both sides of a token’s buying and selling process.

The announcement of the first official Kucoin platform IEO sale, as well as general hype surrounding the prospects of exchange tokens, has galvanized price and trading activity of Kucoin-shares. KCS has risen ~300% since March 1st, from ~USD 0.44 to currently trading ~USD 1.32 while KCS daily reported trading volumes have risen by over 500%.

With the first Kucoin Spotlight token set to occur on April 3rd, price action and trading volume may continue in the short term. However, there is likely to be some profit taking from KCS who have likely benefited from the already significant price growth that has occurred in the last few weeks, so corrections may occur.

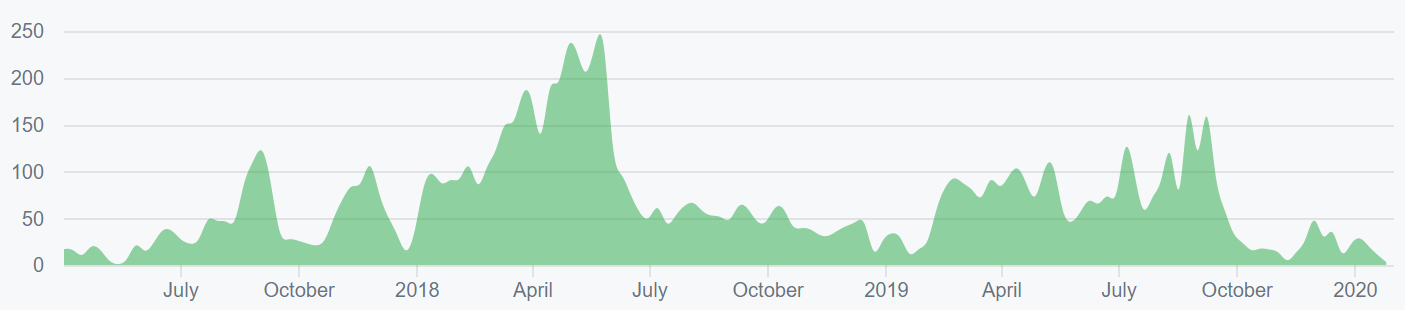

Kucoin Bonus

Source:https://stakingrewards.com/asset/kcs

Interestingly, while the USD price of Kucoin-shares has jumped in the last month, the Bonus reward rate has dropped sharply. This suggests that total transaction volume on the exchange has fallen since around the 10th of March.

This is a bearish short term flag, suggesting that if a price correction does come following the March price pump, resistance against it may be weak considering that falling rewards rates means less incentive to hold onto KCS.

Overall Kucoin volume vs price

Another useful way to assess the token value of KCS, is to connect its price to the performance of the underlying Kucoin exchange, because KCS derives most of its economic value from the redistribution of total daily trading volumes and the quarterly buyback. Thus if the Kucoin platform as a business performs well KCS is worth more.

There are also other speculative considerations. For example, if the market observes the Kucoin exchange sits at the top of crypto exchange rankings as per reports like the TIEs on fake volume on exchanges, this may nudge traders to gamble on the token because of percieved robustness of the Kucoin exchange.

A metric used to assess the relationship between an exchange based token, and volume of the underlying exchanges was suggested by data scientists at Coinfi. Token value/exchange volume, or TVEV, is calculated using the ratio of token value (market cap) divided by 24hr exchange volume.

Historically it appears that a rise in total exchange volume vs token value (falling TVEV line) has been an indicator for upcoming forward or stable price movement. The TVEV line is currently rising quickly, unsurprising given the recent sharp rise in price and subsequently token value (market cap), suggesting a potential correction in KCS price in the near future.

However, historically suggested inflection points for KCS tend to be around 9 points and given that TVEV is currently 6 points, price may have some space to grow before the mismatch in fundamentals and external puts more severe downward pressure on price.

KCS Exchange volume vs Price

Even though KCS functions as a ERC-20 smart contract token built on the Ethereum blockchain, most transactions of the token happen off-chain. This is by design, as much of the token’s transaction functionality is derived from primarily off-chain operations such as utility as a base pair to onramp onto a variety of crypto tokens, and distribution of Bonus payments.

This means that onchain transaction volume patterns are generally erratic for the network, making a traditional NVT signal difficult to use as an indicator for future KCS price movements.

For this reason 24 hour KCS exchange volume is a better option than onchain transaction volume as comparison tool vs external token value

The network value-exchange transactions NVET signal, represents the utility/consumer product like value proposition of KCS. The rationale for using exchange volume as a utilization indicator being that the more KCS that is transacted across exchanges, the more it is utilized for inherent functions such as being an onramp onto other crypto pairs and is being collected by traders to be used to access IEOs.

Source: Bravenewcoin.com

There has been a sharp drop in the NVET of KCS beginning around Mid-February and this is a bullish signal. This means that usage of KCS on Kucoin (KCS is only available on Kucoin) has grown heavily vs token value in the short term and suggests that the ongoing price run is based on fundamentals and that Kucoin-shares are being used.

Currently the Kucoin exchange’s top three pairs are also all KCS pairs (KCS/ETH, KCS/USDT and KCS/BTC). The overall crypto markets most popular trading pair, BTC/USDT, is only the 9th most popular pair on Kucoin while ETH/BTC is the 10th

This unique pattern of falling overall exchange volume vs rising KCS pairs volume, suggests that Kucoin is becoming a niche, contained marketplace where users are focused on trading the exchange’s membership which has no utility outside of the exchange.

The pattern also suggests that the token’s value profile may be changing to being less about a way to access overall trading fees on Kucoin in a co-operative style model, to being a membership token to access IEOs and overall liquidity on the exchange.

Exchanges and trading pairs

The most popular trading option for KCS is ETH, handling close to 35% of daily trading volume. The second and third most popular market are KCS/USDT and KCS/BTC pairs and together the three pairs make up over 99% of daily trading volume.The USD value of daily volume of the entire KCS market is ~ USD 13 million.

The only platform to trade KCS is the native Kucoin exchange. While the usual suspects USDT, BTC and ETH are the most popular options to trade BNB, there are a number of other pairs available for KCS including XRP, EOS, NEO and LTC.

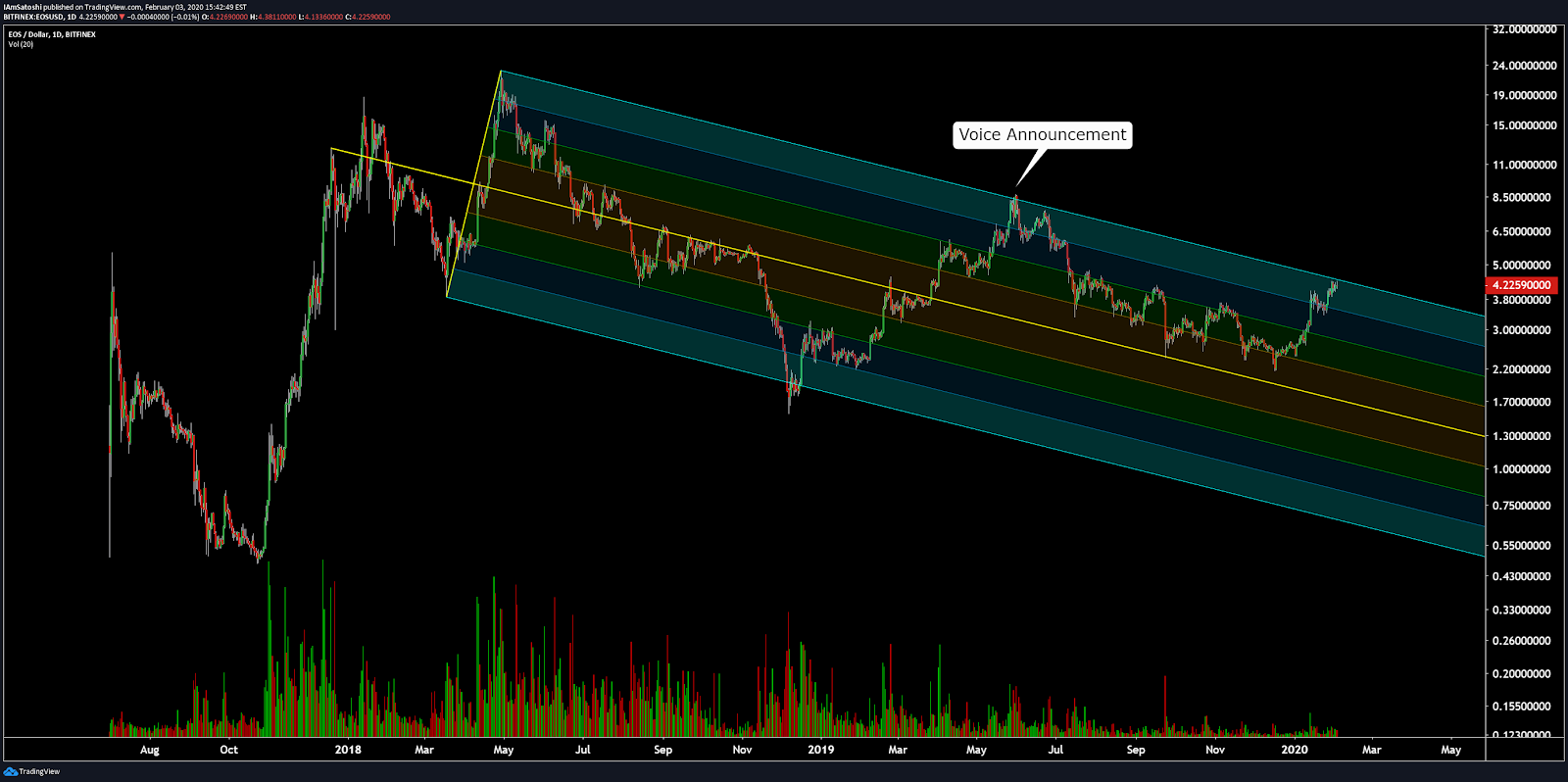

Technical Analysis

Moving Averages and Price Momentum

On the 1D chart, KCS has followed a negative trend since 2018; even with the most recent surge in price that began at the beginning of March 2019. The negative trend has allowed a death cross to persist into 2019.

However, with the recent uptrend, price has broken above the 200 day MA on the 1D chart, which further confirms short-term bullishness. Furthermore, these bullish price movements have resulted in a strong golden cross on the 2 hour chart.

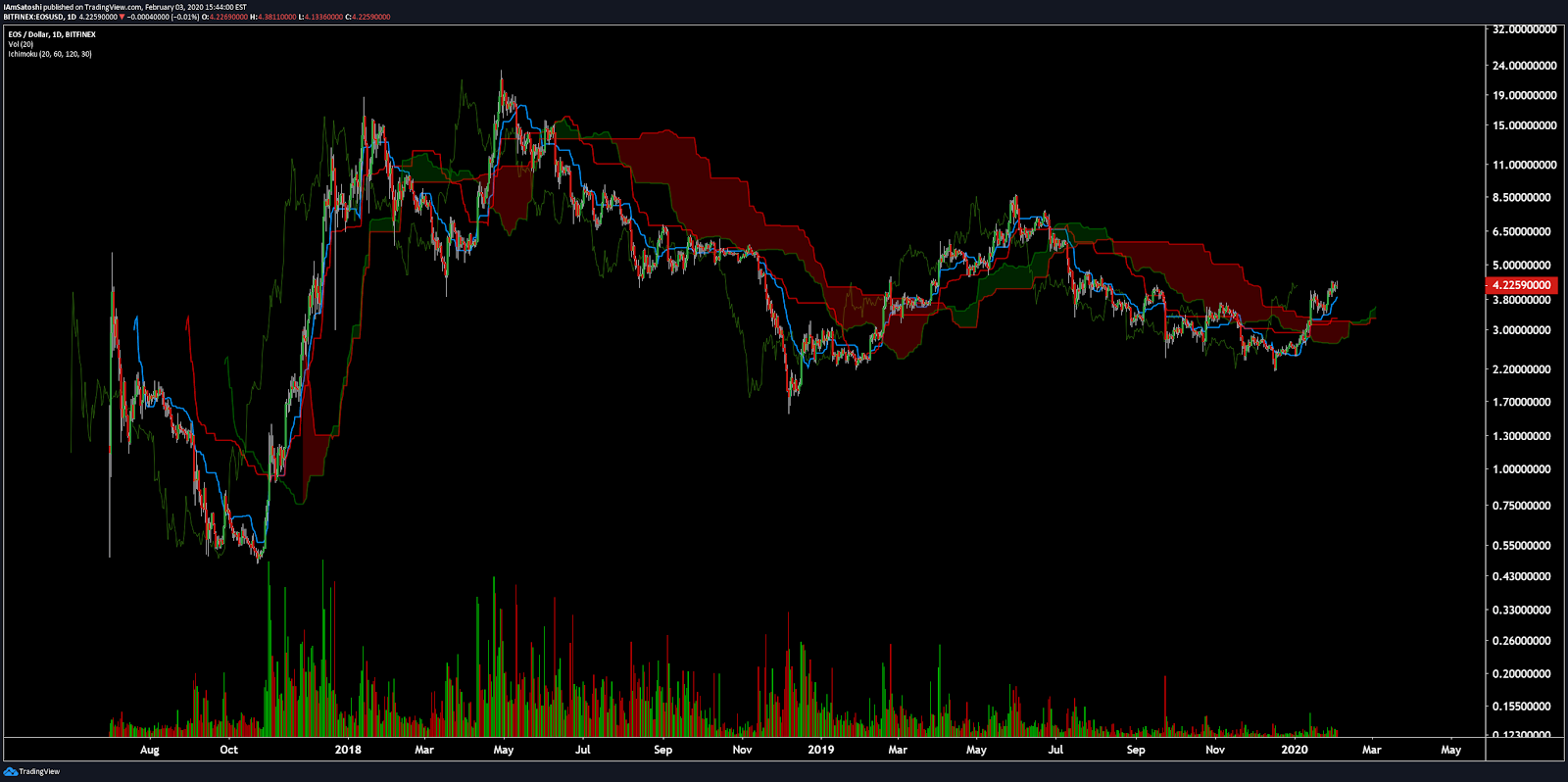

Ichimoku Clouds with Relative Strength Indicator (RSI)

The Ichimoku Cloud uses four metrics to determine if a trend exists; the current price in relation to the Cloud, the color of the Cloud (red for bearish, green for bullish), the Tenkan (T) and Kijun (K) cross, Lagging Span (Chikou), and Senkou Span (A & B).

The status of the current Cloud metrics on the 1D frame with singled settings (10/30/60/30) for quicker signals is mixed; price is above the Cloud, Cloud is bearish, the TK cross is bullish, and the Lagging Span is above Cloud and price.

A traditional long entry would occur with a price break above the Cloud, known as a Kumo breakout, with price holding above the Cloud. From there, the trader would use either the Tenkan, Kijun, or Senkou A as their trailing stop.

KCS completed a Kumo breakout on March 20th and it still remains intact despite RSI being heavily overbought at the moment. Given this notion, price may begin to deflate in the near term, with the ideal scenario being that Cloud support levels of USD1.11 and USD0.96 maintain the breakout and ignite another leg upward. If the aforementioned does occur, price targets are USD1.55 and USD1.67.

The status of the current Cloud metrics on the 1D time frame with doubled settings (20/60/120/30) for more accurate signals is mixed; price is above the Cloud, Cloud is bearish, the TK cross is bullish, and the Lagging Span is above in the Cloud and above price.

The slower settings present a similar analysis as the faster settings. Price is currently maintaining a Kumo breakout, but it’s RSI metric shows overbought conditions. Given the RSI metric, price may deflate towards Cloud support levels before beginning to move higher once again. If Cloud support holds the existing breakout, price targets are USD1.65 and USD1.87.

Conclusion

Kucoin’s native KCS and other exchange tokens, have burst into relevance within the crypto sphere as onramps to access the space’s most exciting new token projects. It has also been given a boost in sentiment following a strong ranking on the TIE’s report on fake volume reported by crypto exchanges, and a platform update in mid February 2019.

The ‘Initial Exchange Offering’ or IEO is a new blockchain buzzword/phrase that has understandable hype. The issuance structure has inherent advantages over ICOs in that it offers immediate liquidity, making tokens that use IEOs appealing for making short term speculative gambles. KCS utility as a membership token to access the Kucoin exchange’s IEO platform has built rapid buying pressure and potentially price and value reassessment from markets. Big picture, KCS still offers a unique co-operative style user reward structure and a share of exchange profits making it a multi-faceted asset.

However, the current price run is likely a bubble and driven primarily by hype for IEOs. This hype may cool down if challenges like infrastructure and regulation are not addressed, while inherent flaws like the lack of self custody may reflect in the value of KCS once the markets learn more about IEOs.

The technical indicators for KCS are bullish in the near term, but a hint of cautiousness is prudent given the current RSI metric. Both the fast-setting trader (10/30/60/30) and slow-setting trader (20/60/120/30), on the 1D chart, will await to see if Cloud support levels of USD1.11 and USD0.96 maintain price’s current Kumo breakout. If so, fast-setting price targets are USD1.55 and USD1.67, while slow-setting price targets are USD1.65 and USD1.87.

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!