A Blockchain can help improve CAC and CLV for Banks

This article is inspired by a question I asked to Bradley Leimer, Head of Innovation at Santander Bank. The question asked the following, "What are the onboarding costs of new customers for banks when opening new accounts?"

This article is inspired by a question I asked to Bradley Leimer, Head of Innovation at Santander Bank. The question asked the following, "What are the onboarding costs of new customers for banks when opening new accounts?" The answer, "In general you’re looking at $150-$400 per checking account – while that seems huge compared to CAC (Customer Acquisition Cost) of a startup, at $10-$40, it’s tough to get people to switch banks."

With CAC being that expensive for banks, it’s not surprising traditional retail banking products are losing money (leaky buckets) at banks. Checking accounts are estimated to have gone from contributing US$12.59 in 1992 to losing US$196.46 in 2012. Debit Card revenue loss is estimated at nearly US$ 8 billion in the United States.

It’s a well known fact that banks are seeking to dramatically cut costs, Deutsche Bank, JPMorgan, HSBC, to name a few. At the same time there is a drive to become more digital, while still trying to acquire and retain end customers. Regulatory oversight has led to steep fines and dramatically increased the cost of service, while also depressing revenue growth. Some of the new regulations banks must follow:

- Basel III

- Dodd-Frank

- Credit Card Accountability, Responsibility, and Disclosure Act of 2009 (CARD Act)

- Regulation E

- FDIC Insurance

- Durbin Amendment

As one can imagine, this is causing banks to assess the Customer Lifetime Value (CLV) for each and every customer across all of their products lines. The main goal is to decrease CAC and increase CLV. Banks now need to look at Profit/Loss Statements for their customers, in order to acquire new customers, retain old customers and expand relationships into other product lines that may be more profitable.

Pascal Bouvier touched on this in his blog Finiculture, when discussing Challenger Banks vs traditional banks. The venture capitalist and aspiring entrepreneur makes some great points on traditional banks biggest problems:

"A challenger bank is in a unique position. As a startup without dependency on a traditional bank, it can focus on customers’ needs from the start, using data tools. A challenger bank is in a position to advise its customers as to which products and services are the most appropriate. Focusing on customers’ needs first and foremost ensures the gap between those needs and product offerings is either miniscule or nonexistent. It also ensures strong engagement – something incumbents struggle with either at a branch or online.”

— – Pascal Bouvier, CFA Venture Partner, Santander Innoventures

The second point Bouvier touches on is that a challenger bank enjoys the benefit of creating its technology from scratch. “From a high level point of view, we are dealing with newish core systems, usually a refresh or newer version of traditional software. Challenger banks also benefit from specialized data hubs that allow them to acquire, analyze, monitor and act on data in a holistic way. Unlike a traditional bank, data does not sit passively in a silo after having been acquired."

I would take this a step beyond just challenger banks, which will still require regulatory approval and proper licensing, while traditional banks are powerful because they sit high around regulatory moat. Challenger Banks are only attacking a few product lines of banks which have recently become less profitable for big banks, fintech startups are also formidable and are attacking specific product lines (payments, remittances, fx, advisory services etc) with appealing digital and technology solutions that are focused on data-driven analytic models.

These models allow them to focus on specific niche markets with laser sharp focus on customer behavior allowing them to acquire customers cheaper, and provide them with ongoing services cheaper. As startups, they also can test new technologies in a much easier and less complicated way. Banks multiple product lines are spread globally in these functional silos, giving the exact opposite effect. Further complexity gets added by things like M&A.

A Cost Cutting World

It is no wonder traditional banks are on the defense and buying into the promise of blockchain solutions. In no particular order, shared ledgers can help banks:

- cut costs- in both the back office and in settlements, FX & remittance

- replace legacy infrastructure

- become more capital efficient and improve liquidity ratios

- reduce redundancies and get rid of operational and functional silos

- reduce regulatory risks

- become more digital/become more like technology companies

- reach finality of settlement

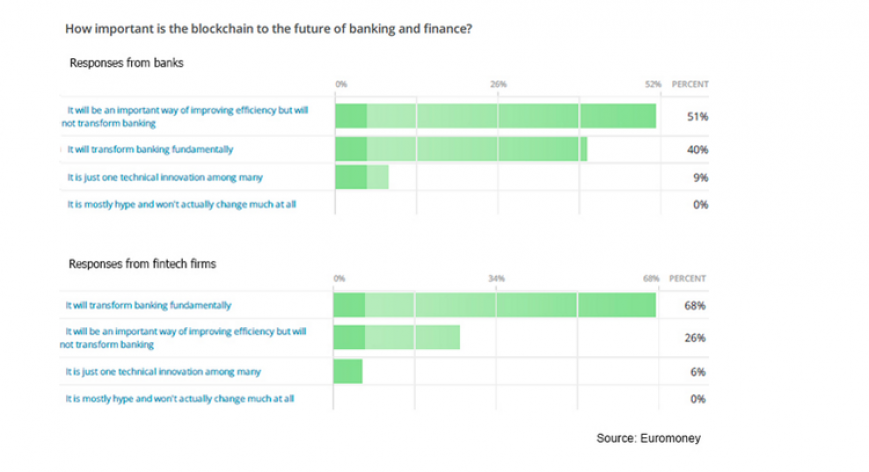

The current popularity of using blockchain is not just a VC Hype Cycle but is also becoming a self fulfilling prophecy on the banking side. Euromoney recently surveyed the banking market to see whats next. Bankers are buying into blockchain in big way, as some of these charts below show.

While most of these are out of the scope this post, bankers are clearly becoming believers in the impact that blockchain can have on their businesses. By adapting shared ledger technology there will also be some "spillover effects for banks," such as decreasing CAC and increasing CLV.

While most of these are out of the scope this post, bankers are clearly becoming believers in the impact that blockchain can have on their businesses. By adapting shared ledger technology there will also be some "spillover effects for banks," such as decreasing CAC and increasing CLV.

Pain Points for Banks in Achieving Lower CAC and Higher CLV

The following are the pain points banks face when trying to figure out CLV that came from Everest Group Research report:

- Silos. Traditional banks offer a variety of products and services that are poorly integrated internally from a operational and systems perspective. Effective CLV analytics requires inputs from multiple systems which is difficult when those systems are different and siloed. this problem is made worse by the non-uniform level of granularity across systems and inconsistent definitions.

- Lack of quality and standardized data. Having a unique customer identifier can be used to track all customer information across all the systems a bank has, and enable creating a single-view of a customer’s history and interactions with the bank. However the underlying systems’ fragmentation makes it hard to get a common customer definition. Moreover banks need to track online behavior to build a forward looking assessment of CLV which is challenging.

- Lack of ongoing feedback mechanisms. CLV analytics need to be fluid and dynamic, as customer profitability calculations are not one-time exercises and need ongoing updates and refinements. In order for the bank to maintain reliable accuracy of these CLV models, a continuous feedback mechanism is required from frontline systems, which is hard to implement.

- Determining "cost to serve" per channel. "Cost to serve" is normally a "one size fits all" average number that is used. However, there are segments of customers who appear profitable based on usage, but when actual cost incurred in servicing is overlaid, they turn hugely unprofitable. The banks therefore need to track customer interaction data across channels and attribute a "cost to serve" interaction, which flows into the Profitability calculation. Channel preference, frequency of interaction and stage of lifecycle are huge drivers of cost to serve and can throw dramatically different results, from what might appear on first glance.

Blockchains Can Help CAC and LTV

Siloed databases are one of the major pain points for achieving proper CLV analysis. When banks implement a blockchain, a shared database gets created, where multiple people can write entries. Assuming banks will used shared ledgers, all nodes will be known and trusted. This allows for consistent definitions, and provides for that elusive unique customer identifier – which is needed to track all customer information across all the systems a bank has, and provides a customer’s history and interactions with the bank. Essentially establishing a chain of custody.

Once this view is established, one can have ongoing feedback mechanisms to understand customer profitability based on customer behavior across all banking departments and services, which in turn will allow for banks to better understand and serve their customers. Not to mention get rid of those annoying calls from multiple departments in a siloed bank asking for the same information.

Planning your 2024 crypto-media spend? Brave New Coin’s combined website, podcast, newsletters and YouTube channel deliver over 500,000 brand impressions a month to engaged crypto fans worldwide.

Planning your 2024 crypto-media spend? Brave New Coin’s combined website, podcast, newsletters and YouTube channel deliver over 500,000 brand impressions a month to engaged crypto fans worldwide.

Don’t miss out – Find out more today