The CBDC Push is here – 3 Questions that Must be Answered

![]()

With Central Banks around the world appearing to move ever closer to the launch of Central Bank Digital Currencies, BNC Founder Fran Strajnar suggests we are sleepwalking into a dystopian quagmire.

The road to hell is paved with good intentions.

For years I have read endless research reports on CBDCs, including the widely referenced BIS report, and more recently the 162 page CitiBank “Money, Tokens and Games” report with a long CBDC section. Hundreds of similar reports have been published.

In all of the literature I have still not found a clear answer for these 3 most important questions;

- Will CBDCs create centrally programmable conditions and restrictions?

- Which problems are CBDCs solving?

- Are CBDCs consolidating Fiscal and Monetary Policy into a single set of hands?

Ultimately the public wants to know if money will still be money.

A) Currently we have cash, where I can take a $10 note and buy a couple of coffees at a café (well maybe only 1 with inflation!). There is no friction. I pull it out of my wallet and since it’s Legal Tender, the vendor accepts payment for goods and services.

B) And we have a multitude of digital payments – online banking, NeoBanks, FinTech solutions etc where users may have a balance and make payments of various types. Currently we live in a society where there are growing safety checks to use these app balances due to compliance, regulation and various treaties.

So what impact will CBDCs have on our current social order impacting A & B?

“Will my life change?” is really the question.

Over the past few years, parallel to the decentralized crypto industry’s hyperbolic growth was a steady stream of Sovereigns and Central Banks exploring Central Bank Digital Currencies.

A slow then sudden rush to explore CBDCs

Led out of the UK Central bank at first, the pilot programs and CBDC efforts have expanded to include 100+ countries now. Having seen CBDCs from the inside go from concept, RFP’s, testing and refinement since inception, I have a unique perspective over its evolution and trajectory.

It’s easier to understand if we break it down into Retail vs Wholesale CBDCs;

Source: From the BIS and quoted in CitiBank’s report.

Conceptually it’s claimed there are these two ways to look at the 100+ Central Banks experimenting with CBDCs.

Wholesale:

It is described that CBDCs will offer a reduction of systemic risk, improved transparency, cost savings to the banking sector which can be passed down to end-users.

So does this mean they will use a public ledger? And the public will be able to see how NGO’s and Government spending is deployed?

Retail:

It is described that CBDCs will be more convenient. Automated taxes, smart-payments and so on.

So does this mean they will use a public ledger? Will the public have the same process as using cash or will every payment be known and permissioned?

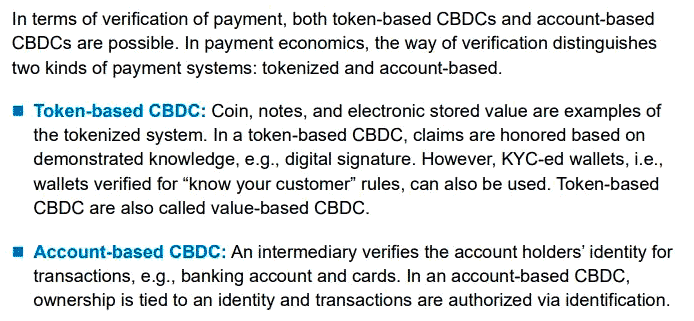

We are told repeatedly in various literature that Privacy will be built in and retail CBDCs in particular are ‘cash equivalents’ but looking at the research it seems that is not the case:

Note the “however” part of the Token-Based description. It seems the feature could exist where you might have a wallet but it is identified and thus restrictions and conditions can be added moving value between users wallets. That is vastly different to my $10 note safely tucked away in my wallet away from prying eyes.

Note the “intermediary verifies” on the Account-Based description, where a 3rd party (be it a regulated regional bank or FinTech) is by technological design and/or legislation enforcing transfers between user-accounts.

If CBDCs for the public are “just like cash” and “privacy will be maintained” that means I’ll be able to send/receive just like walking my $10 note into a café – Right? Money is still money right?

Since much of the literature references the Bank of International Settlements, let’s take a look what Augustin Carstens – GM Of BIS has to say:

Augustin Carstens

Quote 1: “The Central Bank will have absolute control over the rules and regulations that will determine the use of that expression of Central Bank Liability (CBDCs) and we will have the technology to enforce that.”

Quote 2: “We don’t know who’s using a $100 bill today and we don’t know who’s using a 1,000 peso bill today. The key difference with the CBDC is the central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability, and also we will have the technology to enforce that.”

This is in stark contrast to the official discussion forums, working groups and research reports I have poured over which perpetually stress that citizens privacy will be assured.

We must ask ourselves some basic questions here;

- “Why would unelected offshore internationalists need to know everything about every transaction everywhere?”

- “What impact on national sovereignty and society at large would occur if regional governments allow unelected internationalists to enforce regional fiscal and monetary policy?”

It seems to be that the literature, peppered with jargon and buzzwords, is wildly different to the open statements made by BIS which most of the Central Bank working groups, research and forums are always referencing.

So there is a disparity here.

The only thing to do is look at real world use cases of CBDC pilot programs to get a sense of what this thing looks like in the wild?

This would be a logical way to get a sense of what to expect, no?

1 – The Digital Yuan

The Digital Yuan is a full expression of technology convergence. It is available through WeChat and other digital payments apps and is fully integrated with the CCP’s Social Credit System, Covid Health Pass and Digital Identity systems.

When a regional bank hit a solvency problem late 2022 and protestors amassed outside of banks demanding their own money, the government ordered all citizens tracked and tagged at those locations to turn their covid status to ‘positive’. Meaning they were suddenly subject and in breach of brutal covid enforcements. Reuters was one of the few media outlets that dared cover the event, reporting that a “China bank protest stopped by health codes turning red…”

Many months later, now, with the rise (from where?) of the “15 minute city” concept, reports are slowly coming out stating that users cannot use their Digital Yuan outside of their ‘districts’.

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!

Brave New Coin reaches 1M+ engaged crypto enthusiasts a month through our website, podcast, newsletters, and YouTube. Get your brand in front of key decision-makers and early adopters in 2026. Limited slots remaining! Find out more today!